See what you learn from certificates of insurance and why you need one from every subcontractor you hire.

It doesn't have to be costly to work with others

Your business may rely on working with other businesses in order to succeed. But that can leave you exposed because you can be held legally liable for damages if they do not have adequate insurance coverage. Doing business with vendors, buyers, contractors/subcontractors, tenants/landlords and suppliers can have implications on your own insurance coverage and pose a serious threat to the financial health of your organization.

To protect your business, it is important for you to work with only those who are adequately insured and can prove that coverage exists. That’s where certificates of insurance apply.

What is a certificate of insurance?

A certificate of insurance verifies that someone wanting to do business with you has adequate limits of insurance and that the insurance is in force and current. Certificates are usually issued by an insurance agent or broker, but also may be issued directly by an insurance company. A certificate is for informational purposes only and is not an actual contract between the certificate holder and the insurance company. A certificate is not a guarantee that the policy does not contain additional exclusions/coverages.

Any contractor should be able to easily obtain a certificate of insurance by contacting his or her agent or broker. Below are real-life situations in which you would want to request a certificate from a contractor, vendor or another party.

Keep the certificate on file

If a policy is set to expire before a contractor’s work is completed, you should request another certificate for the renewal policy.

Make sure to review the certificate

Insurance requirements will often be written into a contract, but you may also want to supply a required insurance coverage form to the contractor or other party (see “Required insurance coverage” section below). Always obtain the certificate before any work is performed. Most businesses require certificates before the contractor can even set foot on their property.

After obtaining the certificate, review it for the following information:

- The name of the insured

- The proper coverage(s) being provided

- The required limits

- The effective dates

- Your name as the certificate holder

Required insurance coverage

Before providing a service or product to you, the party with whom you are doing business must provide a certificate of insurance that names you as the certificate holder and meets the minimum requirements listed below.

Please note: If the other party either does not provide you with a certificate of insurance or if they provide one with limits lower than the requested minimums, you should discuss this with your agent before work begins.

General liability – $1 million each occurrence/$2 million general aggregate/$2 million products and completed operations aggregate; $1 million personal and advertising injury each occurrence.

Workers' compensation and employers' liability – $100,000 bodily injury by accident, each accident; $100,000 bodily injury by disease, each employee; $500,000 bodily injury by disease, policy limit.

Auto – $1 million CSL (combined single limits)

Umbrella liability – $1 million each occurrence.

For an explanation of how these limits would be applied in the event of an actual loss, consult with your agent.

What you can learn from a certificate

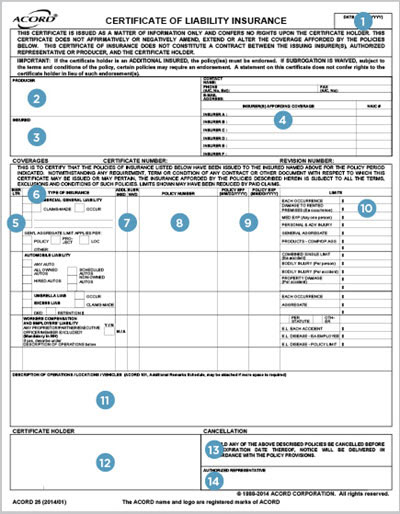

Most certificates of insurance are issued on an ACORD 25 form, a standard form used by the insurance industry. Here’s a brief description of each section of the form, with a sample to review (below):

Identification section

This section identifies the agent/broker, the insured and the insurance company providing coverage.

- 1 - The date the certificate was issued by the agent/broker or insurance company.

- 2 - The name of the insurance agent/broker. Their address, contact name and phone number should be listed in case you need to ask additional questions or confirm coverage.

- 3 - The name of the insured. Be sure to verify that it is an exact match to the name of the person or company you are hiring.

- 4 - The names of insurers. One insurer often provides insurance for all coverages, but at times, different insurers are used for different policies.

Coverages section

This section lists the names of the insurers by coverage provided. Make sure the insurers meet your minimum requirements for financial strength and are reputable carriers.

This section lists the names of the insurers by coverage provided. Make sure the insurers meet your minimum requirements for financial strength and are reputable carriers.

- 5 - The insurer for a particular coverage, keyed to the corresponding letter in item 4.

- 6 - The type of coverage. Ensure that the person or company you are hiring has, at a minimum, general liability and workers’ compensation insurance.

- 7 - Additional insured column. Verify that a “Y” appears to indicate you have been added as an additional insured for ongoing and products/completed operations. A best practice is to ask for copies of the additional insured endorsement to ensure that coverage complies with your insurance requirements.

- 8 - The policy number. Identifies the number of the policy in force between the policy effective date and expiration date listed in the next two columns on the form.

- 9 - The policy coverage dates. Check these to ensure they cover the period in which work will be performed. If a policy is set to expire before the job is completed, request another certificate for the renewal policy.

- 10 - Coverage limits. Make sure the limits held by the contractor meet the limits you require.

- 11 -Description of operations/locations/vehicles. Make sure you understand the meaning of any comments made here and how they may impact your project’s insurance program.

Certificate holder section

This section lists the names of the insurers by coverage provided. Make sure the insurers meet your minimum requirements for financial strength and are reputable carriers.

- 12 - Identification of certificate holder. Make sure your company’s name appears here.

- 13 - Notification procedures if the policy is canceled. Ask to see the policy provisions or endorsements regarding how notice will be given, to whom, and how many days of advance notice will be provided. Make sure they meet your contract requirements.

- 14 - Signature of authorized representative. Make sure the certificate is signed here by the agent or other individual representing the person or company you are hiring.

To learn more about certificates of insurance and why they are important to your business, contact your agent today.